Structuring Hybrid Equity/Debt Deals

Hybrid equity/debt deals are becoming more practical as traditional financing methods don’t always work on their own. In a higher interest rate environment, relying purely on debt can feel too restrictive, while raising only equity can dilute ownership more than desired. Hybrid structures sit in the middle, offering a more balanced way to get deals done (Forbes, 2025).

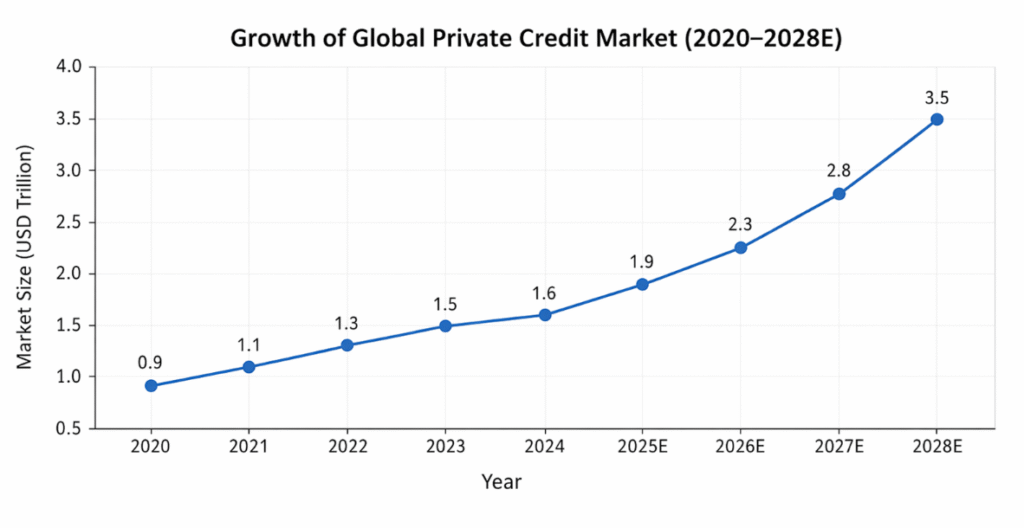

The global private credit market, in which most hybrid instruments sit, has grown to over USD $1.6 trillion (2024) and is expected to reach roughly $3.5 trillion by 2028 (Morgan Stanley, 2025).

Source: Morgan Stanley, 2025

The growth of the private credit market hasn’t followed a straight path. It’s picked up sharply since 2022, largely driven by tighter bank lending and a growing need for more flexible funding options.

Global bank lending growth to corporates has slowed materially since 2022, while private credit has filled the gap, accounting for an estimated 15-20% of leveraged loan issuance in the US market. That shift helps explain the rising use of hybrid equity/debt structures, which naturally fit within this fast-growing part of the market (Ma Financial, 2026).

Structured hybrid equity is a tailored financing solution that combines features of both debt and equity. It allows companies to raise capital while giving investors more downside protection than they’d typically get with standard equity (Capstone Partners, 2025).

It typically sits below senior debt but above common equity in the capital structure. Its main features include a customised structure, some downside protection, less dilution for existing shareholders, and the potential for higher returns.

What is a hybrid equity/debt deal?

A hybrid equity/debt deal features both debt and equity in one structure. It is designed to give capital providers a more protected position in comparison to ordinary shareholders, whilst still allowing them to participate in value creation beyond normal cash interest coupon (Investopedia, 2025).

Hybrid instruments are widely used in private markets, where over 60% of deals are now structured with some form of flexible or non-traditional capital component, particularly in growth equity, mezzanine, and preferred equity transactions (IQEQ, 2026)

In simple terms, hybrid capital usually includes some mix of fixed or floating cash returns, payment-in-kind features, preferred distributions ahead of common equity, conversion rights into shares, warrants or equity kickers, board rights or enhanced governance protections, and covenants that are lighter than senior debt but stronger than ordinary equity (Investopedia, 2025).

The result is a structure that can be tailored to the exact problem a company, sponsor, or borrower is trying to solve.

Where hybrid structures sit in the capital stack

Hybrid structures are especially relevant when a company needs growth capital, liquidity support, refinancing flexibility, or an alternative to a full equity raise.

Hybrid capital usually sits above common equity but below senior secured lenders. In typical leveraged structures, senior debt may represent 50–70% of total capital, with hybrids and mezzanine instruments often filling a 10–30% gap depending on risk profile and cash flow stability (r2 Advisors, 2025).

Why Companies and Sponsors use Hybrid Structures

The main reason companies and sponsors utilize hybrid structures is flexibility and capital efficiency. In leveraged buyouts, for example, sponsors often aim to keep equity contributions below 40–50% of total deal value, using hybrid instruments to bridge funding gaps without over-leveraging the business (Gunung Capital, 2025)

Hybrid structures also help reduce immediate dilution. In equity-only raises, ownership can be diluted by 20–60% depending on the company’s valuation stage, whereas structured hybrid instruments can significantly limit this impact. In addition, they can support refinancing activity by providing flexible capital solutions that bridge funding gaps without requiring a full equity raise (Dups, 2026).

Global refinancing risk has increased, with over $2 trillion in leveraged loans and private credit due to mature between 2025–2027, creating demand for extension and restructuring solutions (Fitch Ratings, 2026).

Why is it appealing to investors?

From the investor perspective, hybrid capital offers a balance between equity upside and downside protection. Private credit has historically delivered higher returns than traditional fixed income, with annualised returns typically in the 7% to 10% range over the past decade, compared to approximately 2.5% to 5.5% for public credit markets (Longangle, 2026).

Default recovery rates for senior secured debt have historically averaged around 60-70%, reflecting their priority claim on assets in the capital structure. Hybrid instruments, such as mezzanine debt or subordinated notes, typically exhibit lower recovery rates due to their junior ranking, but compensate investors through higher yields and potential equity upside (Invesco, 2022).

The main types of hybrid equity/debt deals

Convertible notes are one of the most common examples. They start as debt but can convert into equity later, usually at a pre-agreed trigger or price formula. These structures are often used in growth companies, venture financing and special situations where the company needs capital now but valuation is hard to fix today (Corporate Finance Institute, 2020).

Preferred equity is another common hybrid instrument. It usually sits above common equity in the distribution waterfall and may include a fixed preferred return, redemption rights, governance rights, or conversion features. This is often used in sponsor-backed deals where the goal is to inject capital without overburdening the business with cash-pay debt (Mayer Brown, 2026).

Mezzanine financing is a more traditional hybrid structure. It is subordinated to senior debt, carries a higher return, and often includes warrants or another form of equity participation. It is commonly used when a company is funding an acquisition, senior lenders will not provide enough leverage, and the sponsor wants to complete the transaction without writing a much larger equity cheque (Investopedia, 2025).

Payment-in-kind notes and structured preferred equity are becoming more common, especially in stressed or transitional situations. Instead of requiring full cash payments straight away, these instruments let returns build up and compound over time, which takes pressure off the borrower in the short term. That kind of flexibility can be really useful when cash flow is tight or uneven. The trade-off, though, is a higher overall cost, since investors are taking on more risk and waiting longer to be paid (Glas Agency, 2025).

Hybrid capital is also increasingly showing up in continuation vehicles and secondary-related transactions. In private markets, these structures are being used as exit or liquidity tools, helping sponsors or asset owners provide partial liquidity without forcing a full sale. That makes them useful not just for rescue financing, but also for portfolio management and strategic capital planning (JD Supra, 2026).

Hybrid equity/debt deals are increasingly relevant across both private market vs public markets, particularly as investors diversify beyond the australian stock market and traditional share market australia opportunities. While listed investments such as australian shares, ETF Australia, and funds like the Fidelity Australian Equities Fund or BlackRock Australian Share Fund provide liquidity, hybrid structures sit firmly within alternative investments, private credit investments, and private equity investment strategies.

For investors building a best investment portfolio Australia, hybrid instruments can complement exposure to equity market investment and private placements, especially in Pre IPO, Early Stage IPO, and upcoming IPOs where valuation uncertainty exists. These structures are often used by investment companies and private credit funds engaged in Capital Raising & M&A Advisory, merger and acquisition, and strategic transaction advisory mandates.

From an individual investor standpoint, understanding how to invest in equity market, opening a brokerage account Australia, or learning how to buy stocks in Australia remains foundational. However, access to private investments and hybrid deals typically sits beyond traditional retail channels, reinforcing the divide between public market participation and institutional-grade opportunities in global portfolio management.

As hybrid capital continues to evolve, it plays a growing role alongside conventional tools used to assess performance and planning outcomes, such as a dividend yield calculator, retirement fund calculator, or capital gains tax calculator Australia, particularly when evaluating after-tax returns and long-term wealth strategies.

The risks

Hybrid structures are proven to be useful, but they are not a perfect solution on many occasions. They can create their own problems if the deal is too aggressive or overly engineered. One risk is complexity, because these instruments can become hard to value and hard to explain.

Another is hidden dilution, since a deal may seem non-dilutive initially but conversion features and warrants can create major dilution later. Refinancing risk is also important, particularly if the instrument has a short maturity or mandatory redemption, because the original problem may simply be delayed rather than solved.

There is also the issue of return stacking. Cash coupons, payment-in-kind accrual, fees, warrants, and control rights can make the true cost of capital much higher than it first appears. Misalignment is another concern. If investor downside protection is too strong, management and common shareholders may end up carrying most of the risk while the hybrid investor captures a disproportionate share of the upside (Thomas A. McWalter, Peter H. Ritchen, 2025).

Happy Investing!

———————————————————————————————————————

Vitti Capital Pty Ltd (ABN 13 670 030 145) is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence number 518031. This communication contains general information only and does not take into account your objectives, financial situation, or needs. Before acting on any information, you should consider whether it is appropriate to your circumstances. We recommend you seek personal financial advice before making any investment decision.

If you have not previously received a copy of our Financial Services Guide (FSG), it is available free of charge by contacting us or via https://vitti.capital/fsg/

Past returns do not always indicate future returns and there is always a risk of loss when trading and investing. Our Privacy Policy is available at https://vitti.capital/privacy-policy-2