Equity Market Investment Strategies for Long-Term Wealth

Building long-term wealth in the stock market usually comes down to sticking to a simple, consistent approach rather than trying to outsmart the market. Investors who focus on a mix of solid, high-quality companies, keep their costs low, and stay invested over time tend to put themselves in a strong position to grow their money.

Equity investment strategies are essentially just ways of investing in shares with a long-term mindset, which is typically over 10 years or more. The goal is growth through rising share prices, reinvested dividends, and the overall expansion of the economy.

Some investors focus on growth stocks, aiming to benefit from companies that are expected to expand quickly. Others prefer dividend-paying stocks for a more consistent income stream. Many also use dollar-cost averaging, which is investing regularly over time in order to avoid trying to pick the perfect moment to buy. And for broad, diversified exposure, exchange-traded funds (ETFs) or managed funds are often a popular and practical choice (The Investopedia Team, 2025).

Over long periods, share markets have generally delivered strong and fairly reliable returns, which is why they’re such a key part of building wealth. For instance, the S&P 500 has returned roughly 10% to 10.5% per year on average since its expansion in 1957 (J.B. Maverick, 2025), or about 6-7% per year after adjusting for inflation. Similarly, Australia’s S&P/ASX 200 has delivered long-term returns of around 9-10% annually, including dividends. Taken together, these numbers highlight a pretty clear trend, which over time, shares have consistently outperformed more conservative assets like cash and bonds, which is why they tend to play such a big role in long-term investment portfolios (Vanguard, 2025).

Long-Term Performance of Equity Markets

The long-term performance of equity markets is the foundation behind most investment strategies. Over time, markets have shown a strong ability to generate returns, largely driven by the growth of the companies within them.

The S&P/ASX 200 has delivered long-term average annual returns of approximately 9-10% per year, including reinvested dividends. While returns vary significantly from year to year, the Australian share market has historically generated strong long-term wealth creation through a combination of capital growth and dividend income.

These returns reflect more than just market movements, as they come from real business growth, including rising earnings, innovation, productivity gains, and broader economic development. As companies grow and become more profitable, that value flows through to investors via higher share prices and dividends (J.B. Maverick, 2025).

That said, these returns are anything but smooth in the short term. Markets regularly go through periods of volatility, sometimes quite severe. During the Global Financial Crisis (GFC), Australian equities experienced a significant decline, with the S&P/ASX 200 falling by approximately 54% from its November 2007 peak to its March 2009 trough. Despite this sharp downturn, the Australian share market eventually recovered and went on to reach new record highs, demonstrating the importance of maintaining a long-term investment perspective during periods of market volatility (Vista Finance Group, 2026).

A further example can be seen during the COVID-19 market crash in early 2020, when Australian equities experienced one of the fastest declines in history. The S&P/ASX 200 fell by approximately 37% between February and March 2020 as investors reacted to the economic uncertainty caused by the pandemic.

However, following significant fiscal and monetary stimulus, the market recovered strongly, eventually surpassing its pre-pandemic levels and continuing to reach new highs in subsequent years. This recovery highlighted the resilience of the Australian share market and the benefits of maintaining a long-term investment strategy during periods of extreme volatility. This reinforces the idea that while equity markets are highly volatile in the short run, they have historically trended upward over longer investment horizons (Forbes, 2021).

This pattern is also evident in international markets. For example, Japan’s Nikkei 225 index reached an all-time high in 1989 before experiencing a prolonged downturn following the collapse of its asset bubble. The index took decades to recover its peak level, only surpassing its 1989 high in 2024. While this demonstrates that recovery timelines can vary significantly across markets, it also highlights that long-term investors who remained invested over extended periods were eventually rewarded, despite decades of stagnation (ELAINE KURTENBACH, 2024).

Another important concept is the equity risk premium, which refers to the additional return investors earn for bearing the higher risk of equities compared to safer assets such as government bonds. Historically, this premium has ranged between 4% and 6% (James Chen, 2025). This excess return compensates investors for volatility and uncertainty, and is a primary driver of why equities tend to outperform lower-risk asset classes over long investment horizons.

The Power of Compounding

At the core of long-term investing is compounding. This occurs when returns are reinvested, allowing earnings returns to be generated not just on original investment, but also on the profits already made. Over time, this leads to exponential growth rather than steady, linear growth (Global Masters Fund, 2025).

At this rate, capital does not grow evenly, it doubles approximately every 7 to 8 years. This means that over multi-decade horizons, the majority of total portfolio value is generated in the later years, not the early stages (Investopedia, 2026). For instance, a large share of total wealth accumulation in a 30–40-year investment period typically occurs after year 20, demonstrating the accelerating nature of compounding.

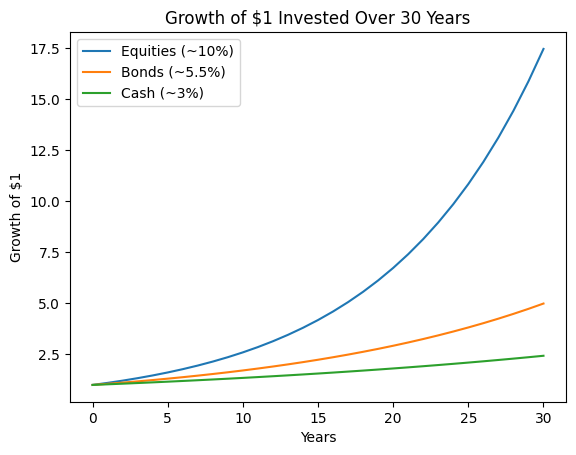

This graph illustrates the power of compounding across different asset classes. Equities, assuming a 10% annual return, grow to approximately $17 over 30 years, significantly outperforming bonds (roughly $5) and cash ( roughly $2.4). This highlights the long-term wealth creation potential of equity markets and the impact of the equity risk premium.

Dividends significantly amplify this effect. Historically, dividends have contributed around 40% of total returns in the S&P 500 (Fidelity, 2026). When dividends are reinvested rather than withdrawn, they generate additional shares, which themselves earn both capital gains and further dividends. This creates a feedback loop where income is continuously converted into additional capital, strengthening the compounding effect over time. Without reinvestment, long-term returns would be substantially lower, highlighting the importance of maintaining full market exposure.

Time is the most critical variable in compounding, and its impact is non-linear. Research on long-term equity performance shows that returns are heavily skewed toward extended holding periods, with volatility smoothing out over time. While short-term returns can vary significantly, the probability of positive outcomes increases materially as the investment horizon extends. Over periods of 10-20 years, the likelihood of achieving positive returns in broad equity indices becomes overwhelmingly high, reinforcing the reliability of compounding when given sufficient time.

Another important dimension of compounding is cost sensitivity. Even small differences in fees can have a large impact on long-term outcomes because they reduce the base on which compounding occurs. For example, a 1% annual fee difference can reduce final portfolio value by more than 20% over multi-decade horizons due to the cumulative effect of lower reinvested returns (Saxo Group, 2025). This is why low-cost investing strategies, such as passive index investing, tend to enhance compounding efficiency over time.

Ultimately, compounding demonstrates that long-term investing success is driven less by timing or prediction and more by duration, reinvestment, and consistency. The combination of steady market returns, reinvested dividends, and sufficient time in the market allows capital to grow exponentially. Investors who remain invested through full market cycles and avoid interrupting the compounding process are positioned to capture the full wealth-generating potential of equity markets.

Diversification and Risk Management

While compounding drives wealth creation, diversification plays a critical role in protecting and stabilising that growth. Empirical evidence shows that concentrated portfolios are significantly more volatile, with individual stocks exhibiting much higher failure rates than the broader market. In fact, long-term studies suggest that a relatively small percentage of stocks account for the majority of total market returns, reinforcing the importance of broad diversification.

This is why investing through indices such as the S&P 500 or S&P/ASX 200 is widely adopted. Data from S&P Dow Jones Indices shows that over 15 years, approximately 87% of Australian active equity funds underperformed the ASX 200, highlighting the difficulty of consistently outperforming diversified benchmarks (Gus Mcclubbing, 2026).

Diversification also reduces downside risk during market stress. Historically, the Australian equity market has delivered around 10.2% annual returns, compared to 6.2% for government bonds, illustrating both the higher return potential and volatility of equities. Including defensive assets alongside equities can therefore smooth portfolio outcomes and improve risk-adjusted returns over time (Tom Kaye, 2023).

Dollar-Cost Averaging and Investment Discipline

Dollar-cost averaging (DCA) reinforces disciplined investing and reduces timing risk. This is particularly important given the variability of returns across shorter time horizons. Historical data shows that even though long-term average equity returns are around 10% per annum, a large proportion of shorter rolling periods deliver returns below this average, highlighting the unpredictability of market timing.

By investing consistently, investors avoid the risk of missing key market rallies. This is crucial because a significant portion of long-term returns is often generated during a small number of strong market periods. Missing just a handful of the best-performing days can materially reduce long-term portfolio performance, reinforcing the value of continuous market exposure.

Happy Investing!

———————————————————————————————

Vitti Capital Pty Ltd (ABN 13 670 030 145) is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence number 518031.

This communication contains general information only and does not take into account your objectives, financial situation, or needs.

Before acting on any information, you should consider whether it is appropriate to your circumstances. We recommend you seek personal financial advice before making any investment decision.

If you have not previously received a copy of our Financial Services Guide (FSG), it is available free of charge by contacting us or via https://vitti.capital/fsg/

Past returns do not always indicate future returns and there is always a risk of loss when trading and investing. Our Privacy Policy is available at https://vitti.capital/privacy-policy-2