Fintech Infrastructure as an Asset

Fintech infrastructure is no longer just the backend plumbing behind financial services. It has become a valuable asset class in its own right, providing the core rails that support the digital economy. Instead of focusing only on consumer-facing fintech apps, investors are increasingly backing infrastructure-led businesses with more durable and defensible revenue models, including banking-as-a-service, payment rails, and regulatory technology (Adyen, 2025).

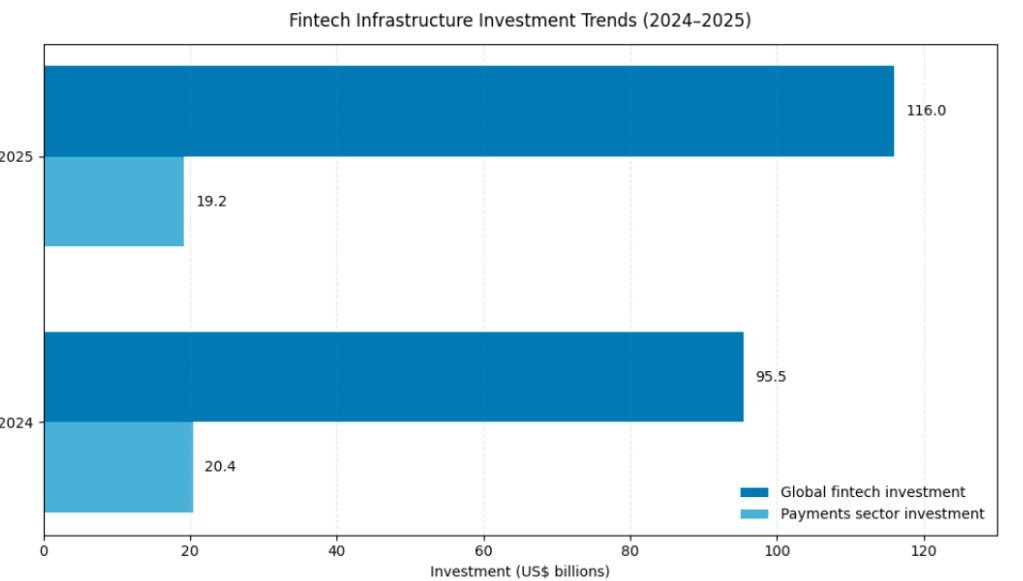

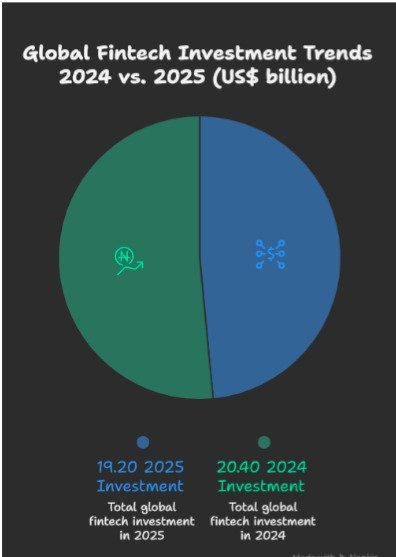

Investors are paying much closer attention to the infrastructure behind these products, the systems that move money, open accounts, verify identity, handle compliance, and connect financial platforms. In 2025, global fintech investment increased to US$116 billion across 4,719 deals, up from US$95.5 billion in 2024, even though overall deal activity was still relatively muted. That suggests the market has become more selective, with capital continuing to flow, but toward businesses with stronger fundamentals and more durable models (KPMG, 2025).

This graph shows that global fintech investment rebounded from US$95.5 billion in 2024 to US$116 billion in 2025, while payments investment remained relatively steady at around US$20 billion, highlighting continued investor interest in core financial infrastructure.

That matters because infrastructure businesses tend to look very different from consumer facing fintechs. They are often more deeply embedded, harder to replace, and more likely to generate recurring revenue over time.

Infrastructure Businesses

One of the main reasons infrastructure is attracting more investor interest is that the revenue is often more defensible.

One reason infrastructure is drawing more investor interest is that the revenue tends to be more durable. Consumer-facing fintech companies often have to keep spending heavily to win and keep customers. Infrastructure businesses are different. Once they are built into payment systems, onboarding workflows, compliance functions, or treasury operations, they often become part of a company’s core operating setup. That can make customers less likely to switch, improve retention, and create steadier long-term revenue (Mason Stevens, 2021).

KPMG’s 2025 fintech data shows this shift quite clearly. Global payments investment came in at US$19.2 billion in 2025, only slightly down from US$20.4 billion in 2024, but the number of deals dropped from 655 to 542, marking a nine-year low. That suggests investors were not pulling away from the space altogether. Instead, they were becoming more selective and directing capital toward larger, more established businesses with stronger fundamentals (KPMG, 2025).

In simple terms, the market is becoming less interested in flashy front-end growth stories and more interested in the businesses that power the system behind the scenes.

Payments Infrastructure

Payments infrastructure is still one of the best examples of why this part of fintech matters so much. McKinsey’s 2025 Global Payments Report estimated that the global payments industry now generates around US$2.5 trillion in revenue and supports roughly 3.6 trillion transactions worldwide. At that scale, the investment case becomes pretty clear. As the movement of money grows larger and more complex, the infrastructure behind it becomes more important and more valuable (Mckinsey, 2025).

Also Read: Alternative Data & Alpha in 2026

Cross-Border Payments

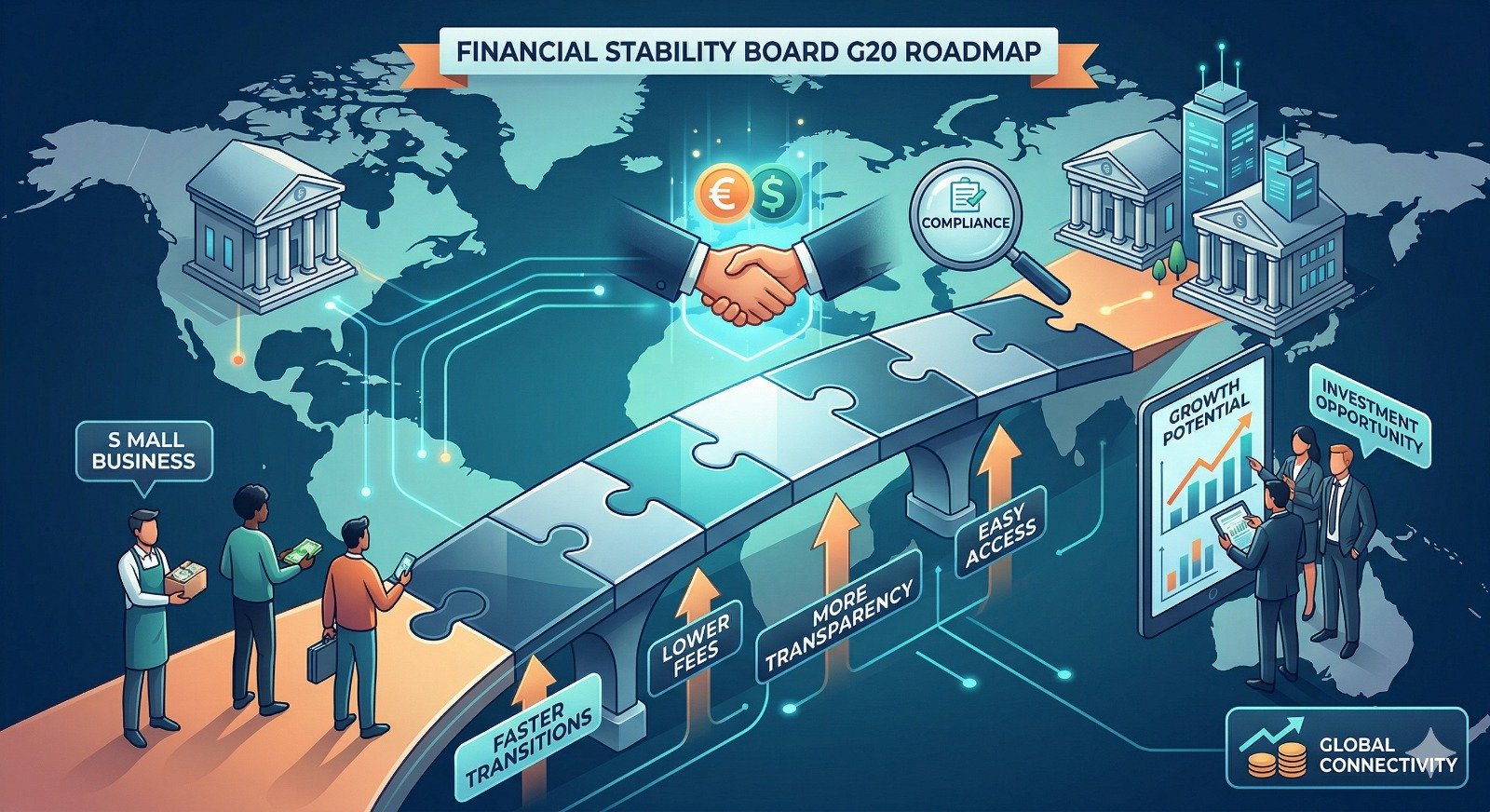

Cross-border payments are another area where the case for infrastructure is getting stronger. The Financial Stability Board said in its 2025 update on the G20 cross-border payments roadmap that the goal is still to make cross-border payments faster, cheaper, more transparent, and easier to access. But it also noted that these infrastructure improvements still need to deliver real benefits for end users. That gap matters. It shows there is already clear demand for better systems, even if the market has not fully solved the problem yet (FSB, 2026).

For investors, that creates a clear opportunity set. Platforms that improve settlement, reduce friction, standardise data, or simplify cross-border compliance are operating in a market where the need is well established and still growing (Trade Treasury Payments, 2026).

Banking-as-a-Service and Embedded Finance

Banking-as-a-service and embedded finance are still important parts of the infrastructure story, but the market is no longer treating every platform the same way.

The stronger businesses in this part of the market are likely to be the ones with reliable bank partnerships, sound compliance systems, and products that genuinely reduce complexity for customers. The weaker ones are more exposed to regulatory pressure, partner risk, and business models that are easier to replicate (The SumSuber, 2026).

That is why investor attention is shifting from the broad idea of “fintech growth” to the much more specific question of which infrastructure layers are truly essential. In the current environment, being part of the stack is not enough on its own. You need to be a mission-critical part of the stack (The SumSuber, 2026).

Australia Shows the Same Pattern

The same trend is visible in Australia.

KPMG’s Australian fintech update for H2 2025 highlighted a softer funding environment overall, but infrastructure-related assets still stood out strategically. One example was Cuscal’s acquisition of Indue for A$49 million, aimed at combining Indue’s payment facilitation capabilities with Cuscal’s existing infrastructure. That is a useful signal of where value is being seen in the market. Even when broader sentiment is cautious, core infrastructure assets can remain attractive because they provide capabilities that are difficult to rebuild from scratch (KPMG, 2026)

That is part of the reason infrastructure assets are increasingly being treated differently from more consumer-facing fintech businesses. They are not just products. In many cases, they are operating layers the wider ecosystem depends on.

Vitti Capital Pty Ltd (ABN 13 670 030 145) is a Corporate Authorised Representative (001306367) of Point Capital Group Pty Ltd (ABN 41 625 931 900), the holder of Australian Financial Services Licence number 518031. The information contained in this website is only intended for the use of those persons who satisfy the Wholesale definition, pursuant to Section 761G and Section 761GA of the Corporations Act 2001 (Cth) (“the Act”).

Persons accessing this information should consider whether they are wholesale clients in accordance with the Act before relying on any information contained. Any advice contained in this communication is general only and does not consider your objectives, financial situation or needs, and you should consider whether it’s appropriate for you. This might mean that you seek personal advice from a representative authorised to provide personal advice.

If you are thinking about acquiring a financial product, you should consider the relevant Product Disclosure Statement or Prospectus (if there is one available) first. Our Privacy Statement is available at www.vitti.capital. Past returns do not always indicate future returns, and there is always a risk of loss when trading and investing.